FTC Charges Arizona Group With Falsifying Incomes on Consumer Credit Apps

According to the regulator, this was the FTC’s first action alleging income falsification by dealerships. Charged are the owners of Tate’s Auto Group, which operates four dealerships in Arizona and New Mexico, near the border of the Navajo Nation.

WASHINGTON, D.C. — Three weeks after announcing the completion of a seven-state sweep regarding compliance with its Used Car Rule, the Federal Trade Commission announced on Wednesday it has charged a group of four dealerships with a range of illegal activities, including falsifying consumers’ income and down payment information on credit applications and misrepresenting financial terms in vehicle advertisements.

According to the regulator, this was the FTC’s first action alleging income falsification by dealerships. Its complaint names Richard Berry as a defendant and Linda Tate as a relief defendant. They operate a group of four dealerships in Arizona and New Mexico, near the border of the Navajo Nation.

“Buying a car is one of the biggest purchases consumers make. When consumers tell an auto dealer how much they make and how much they can pay upfront, the dealer can’t turn those facts into fiction,” said Andrew Smith, the FTC’s recently confirmed director of its Bureau of Consumer Protection. “The FTC expects auto dealers to be honest with consumers from the first advertisement to the final purchase.”

Since at least 2014, according to the complaint, Tate’s Auto allegedly increased its sales by falsifying consumers’ monthly income and down payments on credit applications and finance contracts submitted to finance sources. The four dealerships named in the complaint are Tate’s Auto Center of Winslow, Tate’s Automotive, Tate Ford-Lincoln-Mercury, and Tate’s Auto Center of Gallup.

The regulator charged that, during the sales process, Tate’s Autos asked consumers to provide personal information — including their name, address, and monthly income — and told them the information would be submitted to financing companies. But instead of using consumers’ actual information, the complaint alleges, Tate’s Auto falsely inflated the numbers, making it appear that applicants had higher monthly incomes than they really did. The dealerships also allegedly inflated the amount of a customer’s down payment.

“We’re not talking about nickel-and-dime discrepancies,” wrote Lesley Fair, senior attorney with the FTC’s Bureau of Consumer Protection, in an Aug. 1 blog post on the FTC’s website. “According to just one of the examples in the complaint, a consumer told Tate’s she had a fixed monthly income of about $1,200, but a Tate’s staffer allegedly inflated it to $5,200 in the paperwork.

“Wouldn’t consumers spot the false information? Not necessarily,” Fair continued. “The complaint charges that the defendants often used tactics that prevented people from reviewing the documents. Tate’s personnel allegedly rushed some consumers through the process; had them fill out forms over the phone or in places like grocery store parking lots or restaurants; or altered the documents after consumers signed them.”

The FTC charged that consumers, many of whom are members of the Navajo Nation, were approved for financing based on the false information the group’s dealerships provided. These consumers, the regulator further alleged, defaulted at a higher rate than qualified buyers.

The FTC also charged in its complaint that Tate’s Auto’s advertising deceived consumers about the nature and terms of financing or leasing offers. For example, the group allegedly advertised discounts and incentives without adequately disclosing limitations or restrictions that would prevent many customers from qualifying for the offers.

The regulator also alleges that Tate’s Auto’s social media ads violated the FTC Act, the Truth in Lending Act, and the Consumer Leasing Act by failing to disclose required terms. The FTC is now seeking an injunction barring the defendants from such practices in the future.

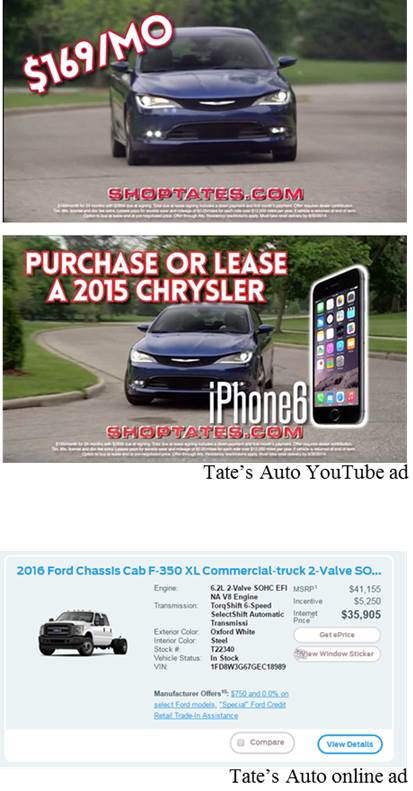

“One YouTube ad claimed the featured car ‘can be in your driveway for only $169 per month,’” Fair wrote in her blog. “In fact, consumers can’t buy that car for the advertised monthly payment. That amount applies only to a lease. What’s more, the FTC says the ad didn’t clearly disclose that to get that monthly payment, consumers must shell out $2,899 plus other fees at lease signing.

“Then there’s the online ad where the company touted an ‘incentive’ discount of $5,250,” Fair continued. “But buried behind multiple hyperlinks was the fact that the discount was available only to consumers who trade in a 1995 or newer vehicle or terminate a lease from another car company 30 days before or 90 days after delivery.”

The FTC’s complaint charges that Berry, acting as owner of the four dealerships, formulated, directed, controlled, had the authority to control, or participated in Tate’s Auto’s allegedly illegal conduct. The FTC also charges that Tate received hundreds of thousands of dollars from the other defendants, including funds directly connected to the alleged unlawful conduct.

“The complaint charges that over time, others in the industry got wise to what Tate’s was doing,” Fair wrote in her blog. “In December 2015, a major financing company that regularly worked with Tate’s conducted a review. The company reported inflated income on 17.9% of applications from Tate’s Auto Center of Gallup, 37.5% of applications from Tate’s Auto Center, 38.7% of applications from Tate’s Nissan Buick GMC, and 44.8% of applications from Tate’s Auto Center of Winslow.”

The Commission vote authorizing the staff to file the complaint was 5-0. The complaint was filed in the U.S. District Court for the District of Arizona.

Originally posted on F&I and Showroom

More Dealer Ops

Ladies and Gentlemen, This Is a Dealership: Why the Fundamentals Still Decide Who Wins

A teaching moment by a legendary football coach happens to apply perfectly in the auto retail space. Learn what it is and how to use it to your store’s advantage.

Read More →

Timing the Market Can Hurt Long-Term Program Performance

For dealer-owned reinsurance entities, avoiding volatility entirely can mean falling behind inflation and missing market rebounds that drive long term surplus growth. Missing just a handful of strong market days can materially impact cumulative returns—an important reminder for long horizon trust and investment strategies.

Read More →

Dealer Ads and the FTC

The agency has made it clear in recent enforcement actions and warnings, in auto retail and other industries, that advertised prices must include all nonoptional costs to the consumer.

Read More →

Used Autos Supply Dwindles

The March shopping surge, despite high prices, cut into inventory by the most since the thick of the pandemic, Cox Automotive analysts calculated.

Read More →

Managing Risk Effectively Through Changing Times

The variables influencing risk pricing have changed significantly over the past five years. Being proactive and responsive to emerging trends is not optional but essential.

Read More →

Survey Reveals What Won't Fix What's Breaking Car Sales

AutoPayPlus says extra-long auto loans are trapping consumers and threatening the dealer trade-in cycle, and that the industry is leveraging the wrong tools to combat high MSRPs.

Read More →

IA American Appoints Two Execs

Senior vice presidents of the company's agent and dealer channels chosen to support general agents and help auto dealers with sales and performance.

Read More →

Cox Automotive Acquires Inspection Firm

Full ownership of Alliance Inspection Management, or AiM, meant to unlock growth for Manheim inspection capabilities

Read More →

Assurant Expands Partnership With Holman

Extended collaboration delivers training, products and performance development to 30 newly acquired Holman dealerships

Read More →

Franchises, Throughput Down in First Half

A handful of states see franchise growth through June, while EV sales per store boost overall business in U.S.

Read More →